The consumer credit space, especially Buy Now, Pay Later (BNPL), is undergoing a rapid transformation. By 2030, the European BNPL market is projected to exceed $300 billion, driven by new user expectations and digital innovation.

But growth brings complexity. To scale responsibly, BNPL providers must solve a strategic trilemma: How to fight increasingly sophisticated fraud, comply with tightening regulations like CCD2, and deliver a seamless user experience all at once.

And at the center of this challenge is one common denominator: identity verification.

The Three Forces Shaping BNPL Today

- Fraud is now industrialized. What used to be isolated attacks are now automated, scalable threats powered by generative AI. Synthetic identities, presentation attacks, and backend injection attacks are not edge cases, they’re everyday realities. In fact, 1 in 20 identity verifications in the financial sector is already fraudulent.According to the AEECF 2025 report, the average amount of fraud in consumer financing is €1,600; in mobile device financing, €750; while the average amount of fraud in vehicle financing rises to €20,000.

- Regulatory pressure is intensifying. The upcoming EU Consumer Credit Directive (CCD2), fully enforceable by November 2026, demands a full overhaul of credit origination processes. Identity verification and traceability will become legal prerequisites—not nice-to-haves.

- User experience is the new competitive baseline. In a saturated market, users no longer ask for security, they assume it. What they demand is speed, simplicity, and results. Any unnecessary step becomes a point of friction and abandonment.

CCD2: The Regulatory Shift You Can’t Ignore

BNPL providers are already navigating GDPR, AML, SEPBLAC, and the ETSI standards. Now, CCD2 adds another layer of accountability and enforcement:

- Wider coverage: Products under €200 and BNPL agreements offered by third parties are now regulated.

- Stricter transparency: Marketing must be clear, fair, and non-misleading, with mandatory warnings like “Borrowing money costs money.”

- Standardized pre-contractual info: The SECCI form must be provided in a clear, mobile-friendly format.

- Algorithm accountability: Consumers have the right to human review and clear explanations of automated credit decisions.

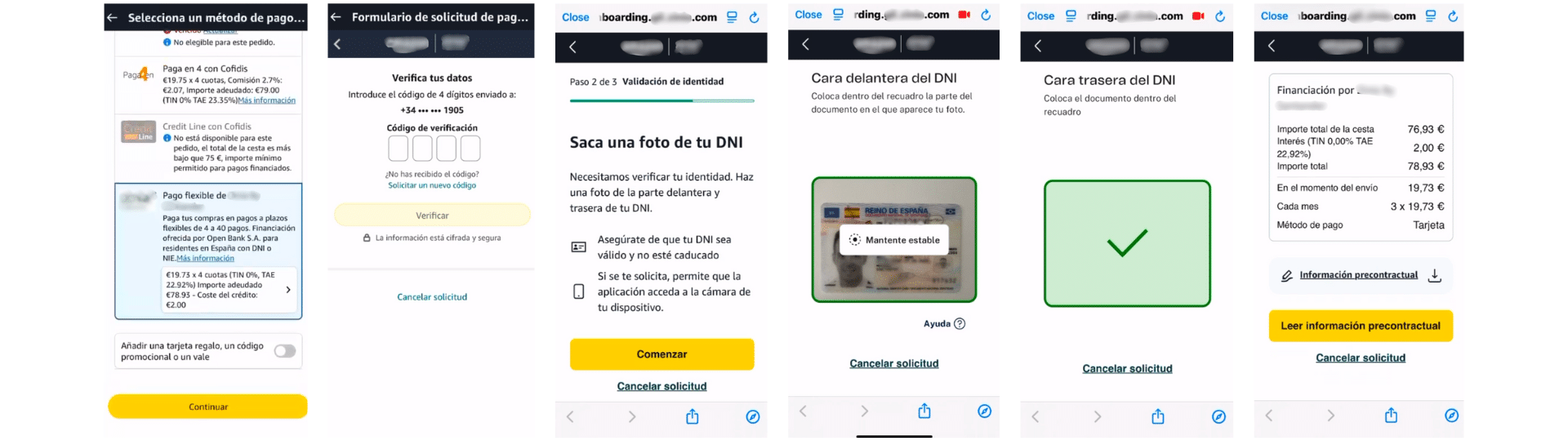

The bottom line? Credit can no longer be offered without identity assurance.

Even if CCD2 doesn’t explicitly regulate KYC, it makes it functionally essential. Real-time, high-confidence identity verification is now the foundation of legal, ethical, and scalable lending.

Why Veridas: Identity as Strategic Infrastructure

Fraud prevention, compliance, and UX don’t need to be trade-offs.

With Veridas, they work together by design.

- Own the stack: Veridas builds and controls its entire tech stack, including biometrics, liveness, document analysis, and injection detection, ensuring unmatched agility, performance, and protection.

- Stop fraud before it happens: Our NIST-ranked facial biometrics, iBeta-certified passive liveness, and injection-resistant architecture block even the most advanced threats.

Compliance by default: We generate full audit trails for every verification step, supporting CCD2, AML, GDPR, and AI Act requirements.

Frictionless, high-conversion UX: Real users are verified in seconds with zero compromise on security.

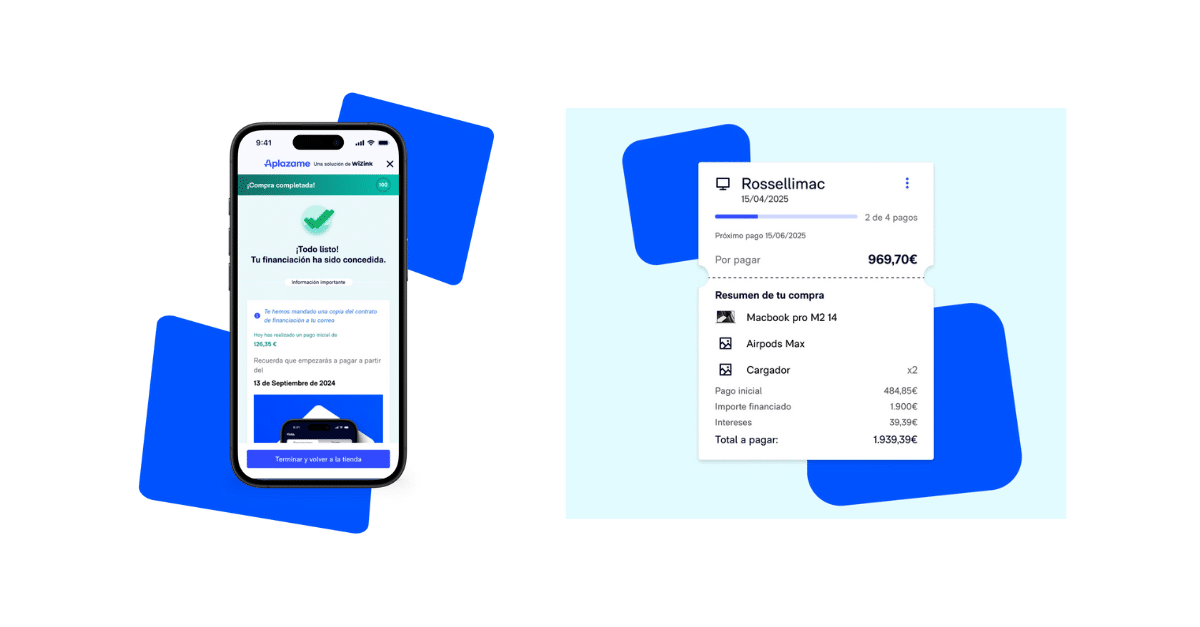

Success Story: Aplazame

Aplazame, a leading BNPL fintech in Spain, needed to scale operations across 1,800+ e-commerce sites, including brands like Iberia, Renfe, and PC Componentes, without compromising conversion or compliance.

With Veridas, identity verification volume grew by 65% in less than a year, while maintaining a zero fraud rate and an average validation time of under 10 seconds, even during peak periods like Black Friday.

“Since implementing Veridas, we haven’t had a single significant fraud attempt. That peace of mind is priceless.” Javier Yuste, CPO, Aplazame.

Strategic Versatility Beyond BNPL

The Veridas platform supports secure identity verification at scale in other high-risk sectors:

- Orange reduced e-commerce fraud to below 1% using Veridas onboarding flows.

- A top global marketplace manages 1.5M+ verifications per year across Spain and Germany.

- A major Mexican telco has processed 7M+ secure identity verifications for device acquisition.

Conclusion: The Future of Credit Starts with Identity

In an industry where growth is digital, fraud is invisible, and regulation is relentless, the advantage isn’t just in the product, it’s in how you verify, protect, and scale it.

Veridas provides the infrastructure to:

- Block fraud before it happens.

- Satisfy the toughest regulatory requirements.

- And deliver a user experience that drives growth.